Avoid These 5 Family Budgeting Mistakes That Can Lead to Long-Term Debt

This post may contain affiliate links which might earn us money. Please read my Disclosure and Privacy policies here

Family budgeting plays an important role in creating financial stability while also helping households manage daily needs and prepare for future goals. A well-structured budget allows families to handle expenses with greater confidence and adjust more easily to changing priorities.

However, maintaining a reliable budget becomes challenging when living costs and financial obligations change. Minor spending habits and overlooked costs can gradually disrupt financial balance over time.

Although these issues may appear manageable at first, they often contribute to financial strain that becomes increasingly difficult to resolve. For this reason, families must regularly evaluate how their financial plans align with their actual spending patterns.

To ensure you make better financial decisions for your family, make sure to be aware of and avoid these common budgeting mistakes:

1) Treating Credit Cards as a Budget Extension

Credit cards can serve as a highly useful financial tool when families use them with intention and discipline. Many households benefit from the convenience they provide, especially when managing cashless payments or handling short-term cash flow gaps between pay cycles.

In this sense, a credit card can support financial flexibility and even help build a positive credit history when managed well.

It’s only when credit shifts from being a payment tool to becoming a regular extension of the monthly budget that challenges begin. Financial pressure increases when families rely on credit cards to cover recurring essentials such as groceries or utilities without a clear repayment plan.

This approach may feel manageable in the short term, but it gradually introduces a cycle where spending outpaces actual income.

Debt accumulation also becomes more likely when balances are carried over from month to month. Interest charges then start to build on unpaid amounts, which reduces the effectiveness of repayments and slows financial progress.

Eventually, families may find that a growing portion of their payments goes toward interest rather than reducing the principal balance.

To maintain financial control, families must keep credit card use for planned spending and make full monthly repayments. This approach allows households to enjoy the convenience of credit while maintaining alignment with their actual income and avoiding unnecessary long-term debt.

2) Ignoring Irregular but Predictable Expenses

Many families build their budgets around monthly recurring costs such as rent, utilities, and groceries. This approach often feels complete at first, yet it overlooks a category of expenses that does not follow a monthly cycle but still occurs regularly throughout the year.

These include school-related payments, home maintenance, and seasonal expenses. The predictable nature of these costs often gets underestimated because they do not appear on a monthly calendar. As a result, households tend to treat them as financial surprises when they arrive.

Financial pressure increases when these expenses coincide with already tight monthly budgets. Some families then rely on credit cards or personal loans to fill the gap, which gradually contributes to long-term debt accumulation.

A more stable approach involves distributing these costs across the year through planned monthly allocations. Sinking funds create a structured way to prepare for irregular expenses, ensuring that they do not disrupt regular cash flow when they occur.

3) Overestimating Income and Underestimating Spending

Budgeting errors frequently begin with assumptions about income and spending behavior that do not reflect actual financial patterns. Many households base their budgets on expected income rather than guaranteed take-home pay, especially when earnings include commissions or overtime.

This optimistic projection creates a false sense of financial flexibility. At the same time, daily expenses often receive less attention during budgeting, even though they consistently impact cash flow.

Small purchases such as convenience meals and transport upgrades appear insignificant individually but accumulate into substantial monthly totals.

Eventually, a gap forms between expected financial capacity and actual spending behavior. This gap often results in end-of-month shortfalls, which families then cover through credit or borrowed funds.

A more accurate budgeting process begins with reviewing actual spending patterns over several months. It provides a realistic baseline and helps align financial expectations with real-life behavior.

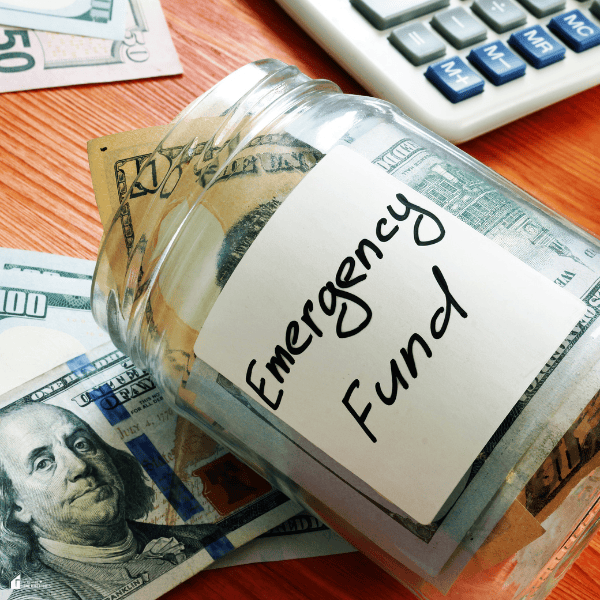

4) Not Building an Emergency Fund

Unexpected financial events occur in nearly every household, yet many budgets fail to account for them. Emergencies such as medical issues or urgent repairs can arise without warning and often require immediate funds.

Without a dedicated emergency fund, families tend to rely on borrowing as a default solution. This reliance introduces debt at the moment of financial stress, which can take a long time to recover from, especially when interest accumulates.

To help stay financially resilient, households must prepare for uncertainty in advance. Even small, consistent savings contributions create a buffer that reduces dependence on credit during emergencies.

Long-term stability improves further when emergency savings are treated as a permanent part of the budget rather than an optional goal. This mindset helps ensure that financial protection grows steadily over time.

5) Not Tracking Small, Everyday Expenses

Small daily expenses often go unnoticed because they seem insignificant when viewed on their own. However, repeated spending on items such as subscriptions and delivery fees can gradually build into a noticeable impact on monthly budgets.

When these expenses remain untracked, financial awareness tends to weaken. The lack of visibility makes it easier to underestimate total spending, which often leads to budget imbalances, especially when small expenses are not reviewed alongside larger financial commitments.

Stronger financial control becomes easier when households implement clear tracking systems for discretionary spending. Categorize your expenses and review them regularly to help your own family gain a clearer picture of where money is actually going and where adjustments may be necessary.

Building Stronger Financial Habits for Long-Term Stability

Long-term debt rarely comes from a single financial decision. Instead, it builds quietly through repeated habits that slowly weaken budgeting discipline and make reliance on borrowed money feel more normal over time.

That said, families must create a budget that allows them to respond more effectively to shifting expenses and changing priorities without losing overall control. When this adaptive approach is sustained over time, its impact will become more significant to your family than any single budgeting adjustment.