How to Get Your Money Ready for Christmas Before December Hits

This post may contain affiliate links which might earn us money. Please read my Disclosure and Privacy policies here

You do not have to be in the Christmas spirit to get your money ready for Christmas.

That may sound strange at first, especially when Christmas still feels far away. You may be thinking about groceries, bills, school costs, gas, activities, back-to-school expenses, or simply making the money stretch until the next paycheck. Christmas may not even be close to the front of your mind yet.

But that is exactly why getting your money ready early matters.

Christmas does not usually strain the budget because of one single thing. It strains the budget because it lands on top of regular life. The mortgage or rent still needs to be paid. The electric bill still comes. Groceries still need to be bought. Gas still goes in the car. Kids still need things. Debt payments, insurance, medical costs, and household expenses do not pause because the holidays are coming.

Then December adds more.

There may be extra groceries, family gatherings, school events, work exchanges, travel, higher winter bills, wrapping supplies, stocking stuffers, last-minute store trips, holiday outfits, baking ingredients, and all the little things that seem small until they happen during the same few weeks.

That is why waiting until December makes Christmas feel more stressful than it needs to be.

Getting your money ready for Christmas is not about rushing the season. It is not about decorating early, shopping before you are ready, or planning every detail months ahead of time. It is about giving your money enough time to handle something you already know is coming.

That matters even more when everyday costs are already putting pressure on families. The Bureau of Labor Statistics reported that the Consumer Price Index rose 4.2% over the 12 months ending in May 2026. Food was up 3.1% over the year, and energy was up 23.5%. When groceries, utilities, gas, and regular household needs are already taking more from the budget, extra holiday expenses can feel even heavier.

A Christmas budget does not need to be perfect. It needs to be realistic. And the earlier you start looking at it, the more choices you give yourself before December arrives.

Why Starting Early Makes Christmas Less Stressful

Starting early gives you one thing December does not give you: time.

When you wait until the holiday season is already here, the money has to come from somewhere right away. That is when people are more likely to reach for credit cards, buy now pay later, bill money, emergency savings, or whatever is available in the moment.

Sometimes that happens because there was no plan. Sometimes it happens because the plan was too late. Sometimes it happens because life was already expensive before Christmas even showed up.

Starting early does not magically make Christmas free, but it does spread the pressure out.

Instead of needing one large amount of money in December, you can start building a smaller amount over several weeks or months. Instead of trying to figure everything out when stores, ads, family expectations, and emotions are all loud, you can make calmer choices before the rush begins.

That is why many people already start thinking about holiday spending before November. The National Retail Federation says that, for several years, about two out of every five holiday shoppers have started browsing and buying before November. The top reasons are to spread out the budget, avoid last-minute stress, and avoid crowds.

That does not mean you have to start shopping right away.

It means you are not wrong for thinking about Christmas money early.

In fact, thinking about the money before thinking about the shopping may be the smarter place to start.

Christmas Money Starts With Your Real Budget

Before you decide how much you want for Christmas, look at what is already happening with your money.

This is the step many people skip because it feels easier to pick a random Christmas savings goal. But a random number does not help if it does not fit your real life.

Look at your current bills. Look at groceries. Look at utilities. Look at gas. Look at any debt payments, medical costs, child expenses, school expenses, repairs, or irregular bills coming up. Look at what months are usually tight and what paychecks are already spoken for.

This is not about feeling bad. It is about being honest enough to make a plan that can actually work.

If your grocery spending has been higher, that matters.

If your electric bill is climbing, that matters.

If back-to-school costs or winter bills are coming before Christmas, that matters.

If your income changes from week to week, that matters too.

A Christmas money plan should fit around your necessary expenses, not compete with them. If the plan only works by ignoring bills, it is not really a plan. It is pressure waiting to happen.

Start with the money reality you have, not the holiday season you wish you could afford.

That may mean your Christmas savings goal is smaller this year. It may mean you save slowly. It may mean you focus on reducing December stress instead of covering every single holiday cost. That still counts.

The goal is not to create a picture-perfect holiday budget. The goal is to keep Christmas from surprising your regular budget all at once.

Count the Paychecks You Have Before Christmas

One of the most useful things you can do is count how many paychecks you have before Christmas.

Not months.

Not a vague “I have time.”

Actual paychecks.

If you get paid weekly, count the weekly checks. If you get paid every two weeks, count those paydays. If you get paid twice a month, count each one. If your income changes, look at the income you can reasonably expect and be careful not to overestimate.

This step helps because Christmas money does not come from the calendar. It comes from income.

Once you know how many paychecks you have, you can ask a better question:

How much can I realistically set aside from each paycheck without hurting my regular bills?

That number may be small.

Small is fine.

If you save $10 from ten paychecks, that gives you $100 you did not have before. If you save $20 from ten paychecks, that gives you $200. If you save $25 from eight paychecks, that gives you $200.

Even if the amount does not cover everything, it lowers the pressure later.

This is where many people get discouraged because they look at the full holiday season and think, “That is not enough.”

But enough for what?

Enough to reduce how much goes on a credit card?

Enough to cover extra groceries?

Enough to keep you from pulling from bill money?

Enough to pay for a few expenses that usually sneak up on you?

A Christmas savings plan does not have to solve everything to be useful. It just has to make December less heavy than it would have been if you started with nothing.

Give Your Christmas Money a Place to Go

Christmas money needs a home.

If it stays mixed in with everyday money, it is too easy for it to disappear. It may go toward groceries, gas, takeout, household supplies, a bill that came early, or one of the many things that pop up during a normal week.

That does not mean you are bad with money. It means the money did not have a clear job.

Give it a job.

You can use a separate savings account, a cash envelope, a budget category, a prepaid card, a sinking fund, or a simple tracker in your spreadsheet. The method matters less than the separation.

When Christmas money has a clear place to go, you can see it growing. You also know not to count it as regular spending money.

This is important because one of the biggest problems with holiday money is that people mentally save it, but never actually separate it.

They think, “I will use part of my next check for Christmas.”

Then the next check comes and regular life uses it first.

A separate category makes the decision more real. Even if you are only moving a few dollars at a time, you are telling your budget that Christmas is coming and that this money has a purpose.

That small habit can change the way December feels.

Make Saving for Christmas Automatic

One thing I like to use for saving is automation.

Automation helps because I do not have to keep making the same decision over and over again. If I already know I want money set aside for Christmas, even a small amount, I can set it up so the money moves before I have time to spend it somewhere else.

That could be an automatic transfer to a separate savings account. It could be a sinking fund. It could be a budget category you fund every paycheck. It could be whatever system you already use to manage your money.

The point is to make the money move on purpose.

This is helpful because money has a way of disappearing when it sits in the same place as everything else. You may plan to save what is left over, but then groceries are higher, the kids need something, gas goes up, or another bill comes in. By the time you look again, there may not be anything left to move.

Automation helps you make the decision once.

It does not have to be a large amount. You can automate $5 a week, $10 per paycheck, $25 a month, or whatever fits your real budget. The amount is not the most important part. The habit is.

When the money moves automatically, your Christmas fund starts growing without needing a big dramatic savings plan. You are not waiting until you feel motivated. You are letting the system help you stay consistent.

And if money gets tight, you can adjust it.

Automation is there to support your budget, not stress it. If the amount you picked no longer works, lower it. If you have a better month, add extra. The goal is not to lock yourself into a number that makes life harder. The goal is to make saving easier to remember.

Pick a Christmas Number That Makes Sense for Your Life

A realistic Christmas money goal is not always the number you wish you had.

It is the number that makes sense for your income, bills, family, and current season of life.

This is where you need to be honest with yourself. Not harsh. Honest.

If your budget is already tight, setting a large Christmas goal may make you feel like you failed before you even started. If your income is steady and you have room, you may be able to set a higher number. If your expenses are changing, you may need to start with a small goal and adjust later.

There is no one correct Christmas budget.

A family with one income will not have the same number as a two-income household. A family with several kids will not have the same number as someone shopping for two people. A family dealing with medical bills, repairs, debt, or job changes will not have the same budget as a family with more breathing room.

Your number needs to belong to your home.

For my family, Christmas is not something we try to go all big on. That is not really our thing, and I know that about us. We still want the season to feel meaningful, but I do not want to create a holiday budget that does not match how we actually live.

But every family is different.

If you love Christmas, love giving, love decorating, love hosting, or this is the season you truly enjoy spending on, then plan for that. There is nothing wrong with wanting a bigger Christmas if it fits your budget and you are preparing for it ahead of time.

The problem is not enjoying Christmas.

The problem is spending like you planned for it when you really did not.

Start with a rough Christmas money goal. Then write down what you already have saved. After that, figure out what is still needed.

The number that still needs to be saved may feel big, so break it down again. What is the next small savings goal?

Not the final goal.

The next goal.

Maybe your final goal is $500, but your next small goal is $25. Maybe your final goal is $300, but your next small goal is $50. Maybe your final goal is simply to have something saved before December, and your next goal is $10.

That is a better way to start because it gives you a number you can act on.

A budget that feels possible is more useful than one that looks impressive but makes you quit.

Think About What Usually Makes December Harder

A good Christmas money plan looks beyond Christmas.

December can be expensive because it is a busy financial month, not only because of the holiday itself.

Think about what usually makes December harder for your household.

Do groceries go up because the kids are home more or because you cook more? Do winter bills rise? Do you drive more? Do school events, class parties, donations, or family obligations pop up? Do you usually have less income because of missed work, slow work, or schedule changes? Do credit card payments from earlier months already take part of your budget?

These are the things that make holiday spending harder to manage.

When you ignore them, the Christmas budget looks cleaner than real life. When you include them, the plan may look smaller, but it becomes more honest.

That honesty can protect you.

For example, if you know winter utilities usually rise, you may decide not to promise every extra dollar to Christmas. If you know groceries are already higher, you may choose a smaller savings goal and focus on avoiding last-minute spending. If you know December usually brings family costs or travel, you may set money aside for that instead of pretending it will not happen.

Getting your money ready for Christmas means looking at the full picture.

Not just the pretty parts of the holiday season.

The real parts too.

Make Room Before the Holiday Pressure Starts

Most families do not create Christmas money because a pile of extra cash suddenly appears.

They create it by making room.

That does not mean cutting every fun thing or making the next few months miserable. It means looking for spending that can slow down so Christmas does not have to be funded all at once later.

Maybe takeout can slow down.

Maybe random store trips can slow down.

Maybe online shopping can slow down.

Maybe convenience spending can slow down.

Maybe subscriptions need a quick review.

Maybe activities that keep adding up need a limit for a little while.

The point is not to shame yourself for spending. The point is to decide what matters before December makes every decision feel urgent.

A small amount redirected now can help later.

If you skip one $20 purchase and move that money to Christmas, that is progress. If you pause a $12 subscription for a few months and move that money over, that is progress. If you reduce one random store trip and keep that money in your Christmas category, that is progress.

These changes may not feel dramatic, but they give your money direction.

That is the part that matters.

When you make room early, you do not have to depend only on whatever is left in December. You have already started building a cushion, even if it is small.

Create a December Money Rule Before You Need It

Holiday spending gets emotional.

There are sales, ads, traditions, family expectations, kids asking for things, memories, guilt, excitement, and the desire to make the season feel special. None of that is wrong. It is human.

But emotional spending can become a problem when there is no rule in place.

That is why it helps to create a December money rule before December arrives.

Your rule may be simple.

You may decide not to use credit cards for Christmas. You may decide not to use buy now pay later. You may decide not to pull from bill money. You may decide not to touch emergency savings. You may decide not to buy last-minute extras just because you feel guilty.

The rule is not there to make Christmas feel strict. It is there to protect your regular budget.

A rule gives you something steady to come back to when everything starts feeling urgent. It helps you decide ahead of time what you are trying to avoid.

This matters because the holiday season can make almost any purchase feel reasonable in the moment.

It is only one more thing.

It is on sale.

The kids would love it.

The family expects it.

Everyone else is doing it.

I will figure it out later.

Those thoughts are common. A money rule helps you pause before they turn into debt, overdrafts, missed bills, or stress in January.

A December money rule is not about being negative. It is about knowing what kind of financial stress you do not want to carry into the new year.

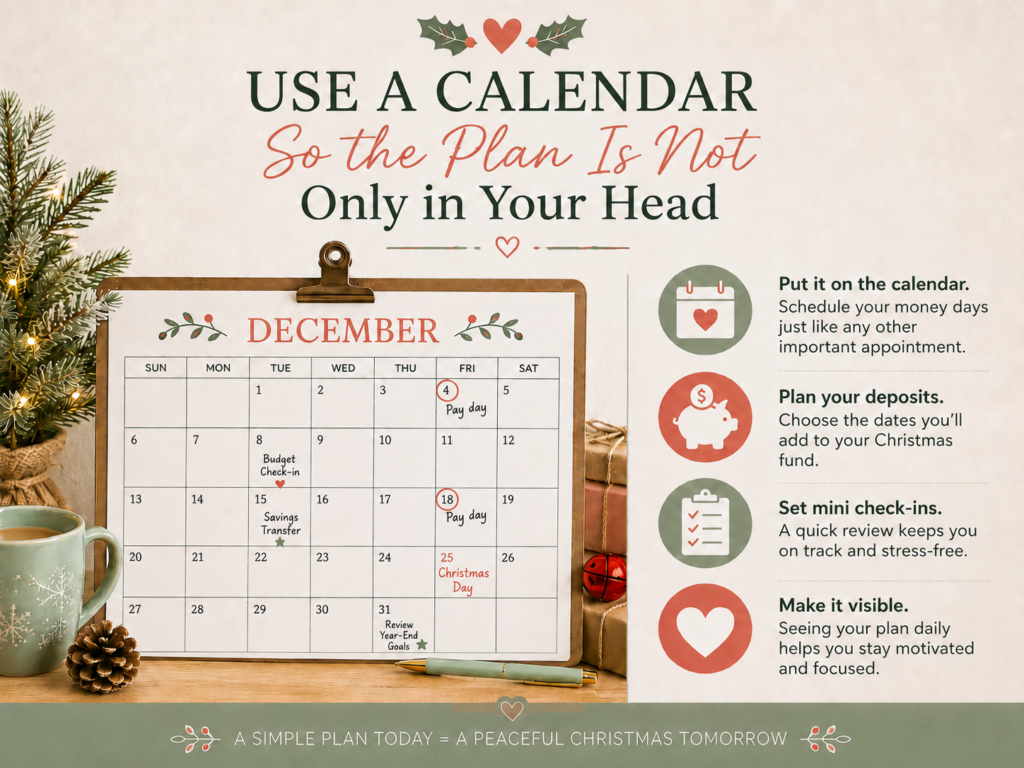

Use a Calendar So the Plan Is Not Only in Your Head

A Christmas money plan is easier to follow when you can see it.

That is why a calendar can be so helpful.

Use a calendar to mark your paydays, bill-heavy weeks, savings transfers, and months that may already be expensive. Write down when you want to move money into your Christmas category. Mark the weeks that are likely to be tight. Mark any known expenses that could affect your savings plan.

This gives you a clear view of the time between now and Christmas.

It also helps you stop treating every month the same.

Some months may be better for saving. Some months may be tighter. Some months may have school costs, insurance payments, car expenses, birthdays, travel, or other things that affect how much you can set aside.

That is normal.

Your Christmas savings does not have to be the same every month to be useful.

One month may be $20. Another may be $50. Another may be nothing because the money truly is not there. Another may be better because you found room somewhere else.

A visible plan helps you adjust instead of giving up.

When everything stays in your head, it is easy to forget what is coming. When you write it down, you can see the pressure points earlier and make better choices.

This is also why counting the months and paychecks matters. The calendar turns “Christmas is coming” into something you can actually plan around.

Do Not Wait for the Perfect Time to Start

A lot of people wait to start getting ready because they feel like they are already behind.

They think they need more money first. They think they need a fresh month. They think they need a perfect budget. They think there is no point starting if they cannot save much.

But waiting for the perfect time is often what makes December harder.

You do not need a perfect time.

You need a starting point.

That starting point can be very small. It can be counting your paychecks. It can be choosing a place for Christmas money. It can be moving $5. It can be writing down your Christmas money goal. It can be looking at one spending habit that needs to slow down. It can be deciding what you do not want to rely on this year.

Those small actions are not wasted.

They help you pay attention earlier.

And paying attention earlier is a big part of getting your money ready for Christmas.

When money is tight, it is tempting to avoid looking ahead because the numbers may not be what you want them to be. But avoiding the numbers does not make Christmas cheaper. It only makes the pressure show up later.

Looking now gives you time to make smaller decisions.

That is the whole point.

What Getting Your Money Ready for Christmas Actually Looks Like

If you have never done this before, keep it simple.

You do not need a complicated holiday binder. You do not need ten trackers. You do not need a perfect savings challenge. You do not need to know every gift, every meal, or every event.

Start with the money.

First, look at your current budget and decide what is realistic. Then count how many paychecks you have before Christmas. After that, choose where your Christmas money will go so it does not get mixed in with everyday spending.

Next, automate what you can, even if the amount is small. Then pick a Christmas money goal that fits your life. It can be a rough number. You can change it later.

After that, look at what could make December harder so your plan includes real expenses, not just the holiday expenses that are easy to remember.

Then choose one spending area that can slow down so you can create a little room. Decide on one December money rule so you know what you are trying not to rely on. Then put the plan on a calendar so you can see your paydays, savings goals, and tight weeks.

That is enough to start.

You can build from there.

The important thing is that you are no longer waiting for December to tell you there is not enough time.

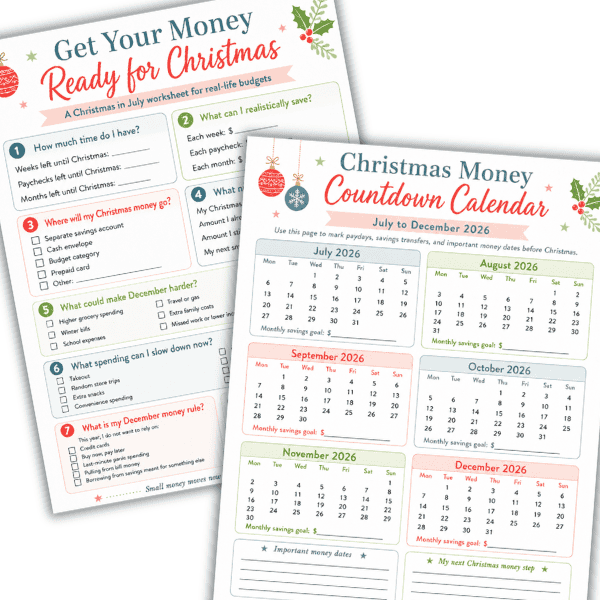

How the Printable Can Help You Put the Plan on Paper

I created the Get Your Money Ready for Christmas printable to help you work through these steps without overcomplicating the process.

The worksheet gives you a place to write down how much time you have, what you can realistically save, where the money will go, what number feels possible, what could make December harder, what spending can slow down, and what rule you want to set for the season.

The calendar helps you see the months leading up to Christmas so you can mark paydays, savings transfers, bill-heavy weeks, and important money dates.

You can use it even if you have never planned ahead for Christmas before.

You do not have to fill it out perfectly. You do not have to know every answer. Start with what you know, then come back to it as your budget changes.

The printable is simply a way to get the plan out of your head and onto paper.

That matters because money feels less overwhelming when you can see the next step.

Give Your Christmas Budget Time to Work

Getting your money ready for Christmas is really about giving your budget time to catch up before the holiday season gets expensive.

It does not mean you have to turn Christmas into a huge event. It does not mean you have to start buying everything early. It does not mean you need to follow someone else’s version of what the holidays should look like.

Your Christmas budget should match your family, your income, your bills, and the kind of holiday you actually want to have.

For some people, that may mean saving for gifts, food, travel, decorations, hosting, and traditions because Christmas is a big deal in their home. If that is you, starting early is even more important because the money needs time to build.

For others, Christmas may be simpler. Maybe you do not go all out. Maybe you focus on food, a few gifts, family time, or just keeping the season calm. That still needs a plan because even a simple Christmas can cost more than a regular month.

The point is not to make Christmas bigger.

The point is to make the money part less stressful.

When you count your paychecks, choose a realistic savings amount, automate what you can, and give the money a clear place to go, you are no longer waiting for December to figure everything out. You are giving yourself time to make choices before the pressure starts.

That matters even more when everyday expenses already feel high. Groceries, utilities, gas, debt payments, and regular bills do not stop because Christmas is coming. If anything, December can make those regular expenses feel heavier because there are so many extra things happening at the same time.

Starting early helps you see that before you are standing in the middle of it.

You may not save as much as you hoped. You may need to change the number later. You may have a month when nothing extra can be set aside. That is real life, and it does not mean the plan failed.

A Christmas money plan is allowed to adjust.

What matters is that you are paying attention before the season starts making decisions for you.

Use the Get Your Money Ready for Christmas printable to write down your numbers, mark your paychecks, choose where the money will go, and decide what spending can slow down so your Christmas fund has room to grow.

You do not need a perfect plan to start.

You need a realistic one that gives your money time.